Double Declining Balance Method / Double Declining Balance Depreciation Template - CFI ... - The double declining balance method is simply a declining balance method in which double (200%) of the straight line depreciation rate is used.

Double Declining Balance Method / Double Declining Balance Depreciation Template - CFI ... - The double declining balance method is simply a declining balance method in which double (200%) of the straight line depreciation rate is used.. Companies can use one of two versions of the double declining balance method: In other words we can say that double declining depreciation method uses double the rate of straight line method. According to international accounting standard (ias) 16 para 60: Using the double declining balance method. The 150% version or the 200% version.

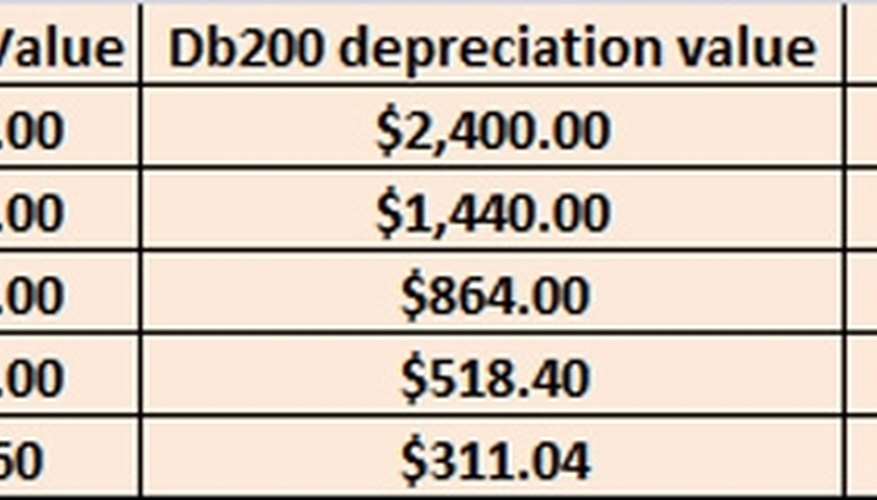

The remaining balance would be the cost minus. Declining balance method is considered an accelerated depreciation method because it depreciates assets at higher rates in the beginning years and lower rates in the later years. The double declining balance (ddb) method is the most commonly used. Rate of depreciation = 100% / no. This method is also known as the 200% declining balance method of depreciation.

How to Calculate 200 DB | Bizfluent from img-aws.ehowcdn.com The double declining balance method of depreciation is used to report depreciation for accounting purposes. Prepare a depreciation schedule using double declining balance method. Double declining balance method and iass. This method is an enhanced form of depreciation that is recognized during the initial few years. Learn how to calculate ddb here. Declining balance method is considered an accelerated depreciation method because it depreciates assets at higher rates in the beginning years and lower rates in the later years. A variation on this method is the 150% declining balance method, which substitutes 1.5 for the 2.0 figure used in the calculation. The declining balance method of depreciation is a form of accelerated depreciation where an asset is depreciated more quickly in the beginning of its useful life.

This method is also known as the 200% declining balance method of depreciation.

The 150% method is appropriate. This method is also known as the 200% declining balance method of depreciation. Double declining balance method and iass. In other words we can say that double declining depreciation method uses double the rate of straight line method. The double declining balance depreciation method is generally used when an asset is depreciating at a faster rate at the beginning of its lifespan or where the organization intends to shift profits further into the future by accounting for larger amounts of depreciation at the beginning of the asset's life span. The double declining balance method of depreciation is used to report depreciation for accounting purposes. It is also called accelerated depreciation. Then we'll cover a full worked example where you'll learn how to apply the double declining method in three simple steps. There are two types of accelerated depreciation. The remaining balance would be the cost minus. The percentage is called accelerator and it reflects the degree of acceleration in depreciation. It is a common form of accelerated depreciation also known as 200 times declining balance method. The double declining balance (ddb) method is the most commonly used.

Here, double means 200% of the straight line depreciation rate. Double declining balance method | definition and example. The double declining balance method of depreciation is used to report depreciation for accounting purposes. Companies can use one of two versions of the double declining balance method: What does double declining balance method mean?

Double declining balance method of depreciation ... from i1.wp.com What is double (200%) declining balance method? Double declining balance depreciation isn't a tongue twister invented by bored irs employees—it's a smart way to save money up front on business expenses. Learn how to calculate ddb here. It is also called accelerated depreciation. The declining balance method of depreciation is a form of accelerated depreciation where an asset is depreciated more quickly in the beginning of its useful life. Double declining balance (ddb) depreciation is an accelerated depreciation method that expenses depreciation at double the normal rate. The double declining balance depreciation method is generally used when an asset is depreciating at a faster rate at the beginning of its lifespan or where the organization intends to shift profits further into the future by accounting for larger amounts of depreciation at the beginning of the asset's life span. It cannot be used to get a tax deduction.

Steps to calculate double declining method are as follows −.

Double declining balance method = 2 * (cost of the asset/useful life). Using the double declining balance method. If you are using double declining balance method, just select declining balance and set the depreciation factor to be 2. In other words we can say that double declining depreciation method uses double the rate of straight line method. The declining balance method of depreciation is a form of accelerated depreciation where an asset is depreciated more quickly in the beginning of its useful life. As the name implies, declining double balance doubles the rate at which you can depreciate your asset compared to the straight line method. Steps to calculate double declining method are as follows −. This involves accelerated depreciation and uses the book value at the beginning of each period as its name implies, the ddd balance method is one that involves a double depreciation rate. There are two types of accelerated depreciation. Double declining balance method | definition and example. Companies can use one of two versions of the double declining balance method: Declining balance method is considered an accelerated depreciation method because it depreciates assets at higher rates in the beginning years and lower rates in the later years. Prepare a depreciation schedule using double declining balance method.

The double declining balance depreciation method is generally used when an asset is depreciating at a faster rate at the beginning of its lifespan or where the organization intends to shift profits further into the future by accounting for larger amounts of depreciation at the beginning of the asset's life span. Using the double declining balance method. This method is also known as the 200% declining balance method of depreciation. The depreciation method used shall reflect the pattern in which the asset's future economic benefits are expected to be consumed by the entity. Rate of depreciation = 100% / no.

Fixed Assets from www.tronia.com It is a common form of accelerated depreciation also known as 200 times declining balance method. The remaining balance would be the cost minus. Rate of depreciation = 100% / no. It cannot be used to get a tax deduction. According to international accounting standard (ias) 16 para 60: The double declining balance depreciation method is an accelerated depreciation method that multiplies an asset's value by a depreciation rate. What does double declining balance method mean? If you are using double declining balance method, just select declining balance and set the depreciation factor to be 2.

Here, double means 200% of the straight line depreciation rate.

With the double declining balance method, you depreciate less and less of an asset's value over time. The double declining balance depreciation method is an accelerated depreciation method that multiplies an asset's value by a depreciation rate. Let's assume that a retailer purchases fixtures on january 1 at a cost of $100,000. Double declining balance method = 2 * (cost of the asset/useful life). Declining balance method is considered an accelerated depreciation method because it depreciates assets at higher rates in the beginning years and lower rates in the later years. This method is an enhanced form of depreciation that is recognized during the initial few years. There are two types of accelerated depreciation. It is a common form of accelerated depreciation also known as 200 times declining balance method. Steps to calculate double declining method are as follows −. The double declining balance depreciation method is generally used when an asset is depreciating at a faster rate at the beginning of its lifespan or where the organization intends to shift profits further into the future by accounting for larger amounts of depreciation at the beginning of the asset's life span. It is also called accelerated depreciation. Prepare a depreciation schedule using double declining balance method. The 150% version or the 200% version.

You have just read the article entitled Double Declining Balance Method / Double Declining Balance Depreciation Template - CFI ... - The double declining balance method is simply a declining balance method in which double (200%) of the straight line depreciation rate is used.. You can also bookmark this page with the URL : https://lasdert.blogspot.com/2021/05/double-declining-balance-method-double.html

Share Awesome

Belum ada Komentar untuk "Double Declining Balance Method / Double Declining Balance Depreciation Template - CFI ... - The double declining balance method is simply a declining balance method in which double (200%) of the straight line depreciation rate is used."

Belum ada Komentar untuk "Double Declining Balance Method / Double Declining Balance Depreciation Template - CFI ... - The double declining balance method is simply a declining balance method in which double (200%) of the straight line depreciation rate is used."

Posting Komentar